https://www.slab.org.uk/faqs/travel-and-subsistence/

https://www.slab.org.uk/faqs/travel-and-subsistence/

The hourly rate for translation and interpreting includes all travel expenses up to the first 60 miles (round trip), including out of pocket expenses e.g. petrol costs or bus fares. No travelling expenses will be paid for an interpreter for a round trip of less than 60 miles to and from the location of the assignment.

Journeys in excess of 60 miles will attract a payment for travelling time and for transport costs as set out below.

All work should be undertaken with due regard to economy and the interpreter’s time should be managed to minimise costs. If more than one client is seen in the location on the same day, any chargeable travelling time and transport costs should be equally apportioned with the number of clients seen.

Where possible interpreters local to the assignment should be used. Where an interpreting firm has branches throughout the country, the work should be performed by the branch nearest to the location of the work.

It is not appropriate to charge travel from a more distant location if the interpreter was on business in another part of the country, thereby passing on travelling costs to other assignments. When assessing an invoice with travel in excess of 60 miles, we will look for the nearest branch office and calculate the travel costs from that office.

However we recognise that there will be situations where this may not be possible due to the availability and location of interpreters. In these situations we will take a pragmatic approach and consider the circumstances.

Any travelling time applicable to journeys in excess of 60 miles (round trip) will be paid at half the hourly rate (£15). Travelling time should be calculated from the contractor’s place of business or the interpreter’s home, whichever is the closest to the place of the assignment. Travelling time should be apportioned equally between all clients seen.

For trips in excess of 60 miles (round trip), irrespective of the mode of transport used, we will pay the most economic method of travel, taking into account the overall costs of tickets/petrol and of travelling time.

The full cost of the journey will be paid regardless of the number of miles. For example, journeys of 100 miles will attract payment for the full 100 miles, not for the 40 miles in excess of the minimum distance.

Where public transport is appropriate, it is paid at standard class rates. The cost of bus tickets and train fares should be apportioned equally between all clients seen and vouching should be produced.

Out of pocket petrol costs will be paid for car journeys. This cost should be apportioned equally between all clients seen.

For ease of calculation we use HMRC advisory fuel rates which represents the fuel costs only. You can view these on their website. HMRC's website is updated every six months in recognition of the fluctuating fuel costs. The fuel costs are based on a car with an engine up to 1400cc. No additional allowance will be allowed for cars with larger engines.

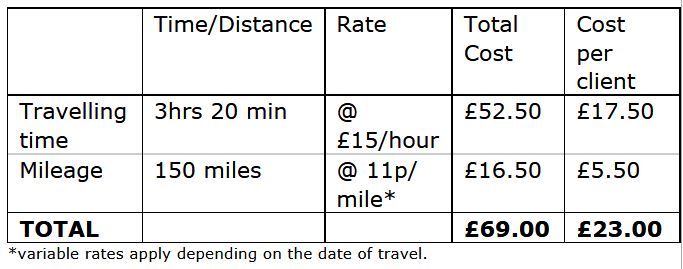

The following is an example of how travelling time and transport costs would be assessed:

Three clients are seen in the same location; having travelled a total of 150 miles the following would be chargeable:

In this example, car travel is the most economic so is used in preference to the train fare.