https://www.slab.org.uk/solicitors/training-e-learning-and-laol/elearning-and-online-guidance/applications/understanding-vat-on-our-applications-system/

https://www.slab.org.uk/solicitors/training-e-learning-and-laol/elearning-and-online-guidance/applications/understanding-vat-on-our-applications-system/

In order that we can ensure that we are paying your accounts at the correct VAT rate we are making changes to our Applications systems.

For new cases created on or after 23 September 2023, you will now be asked to clarify whether your client is a non-UK resident.

More information on how we treat VAT can be found in our detailed legal aid guidance.

Legal services provided to clients who do not have a right to stay in the UK, with a few minor exceptions that are unlikely to arise in the context of legal aid, are deemed to be supplied to them in their country of origin.

For VAT purposes, people who have not been granted a right or permission to remain in the UK should be treated as belonging in their country of origin.

This will apply to, for example, asylum seekers and those entering the UK without permission.

This places the legal services outside the scope of UK VAT and VAT is not chargeable on those accounts.

The legal services which would not be eligible for payment with VAT include:

Although you could provide legal services to clients who do not have a right to stay in the UK, in any type of advice and assistance, ABWOR or legal aid case it is recognised that this is far more likely to occur in certain types of case than others. For example, you will frequently be providing legal services to clients who do not have a right to stay in the UK in the following types of case:

It is your responsibility to establish and be satisfied that your client has a right to stay in the UK.

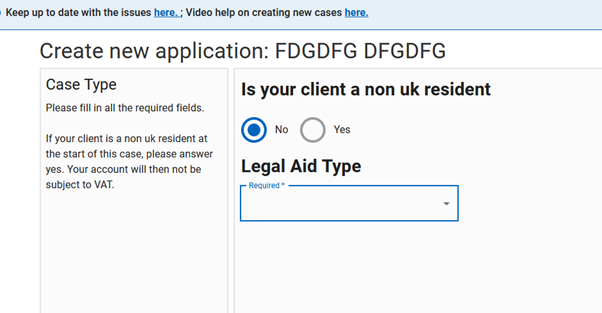

When you create a new application for any form of advice and assistance, ABWOR or legal aid you will now be asked to answer the question: “Is your client a non-UK resident?”

The question will default to “No”.

If your client has not been granted a right or permission to remain in the UK then you must answer “Yes” to this question.

This is a compulsory question and you cannot proceed further until this has been answered.

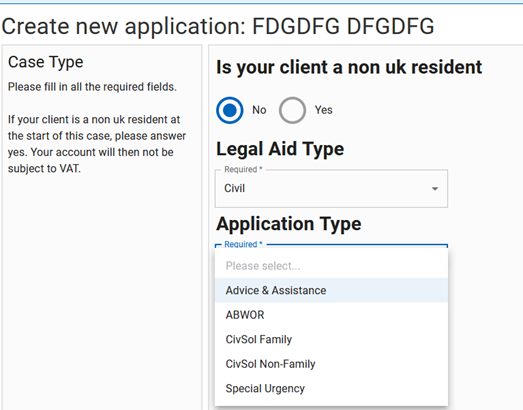

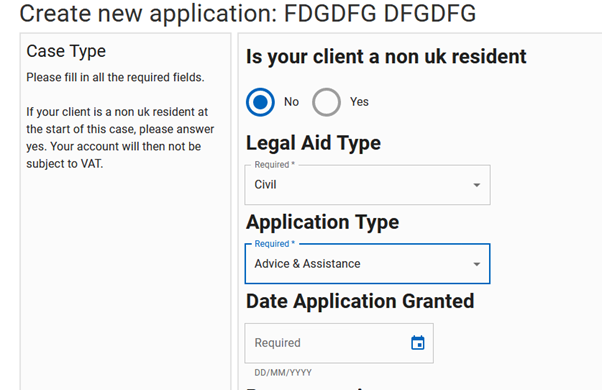

You should:

Once the application type has been selected, complete the date application field is submitted, or granted, as the case may be and then continue with your application in the normal manner.

As part of the Applications update, all current Advice and Assistance and ABWOR cases with a category of “ASY” (Asylum), including those where an interim claim has been submitted, will automatically be updated with the client’s residential status set to non-UK.

This will mean that any subsequent claims that are made in will no longer have VAT added.

Unless we are otherwise informed we will pay all subsequent accounts as VAT exempt, so it is essential that you check that the update that has been applied is correct.

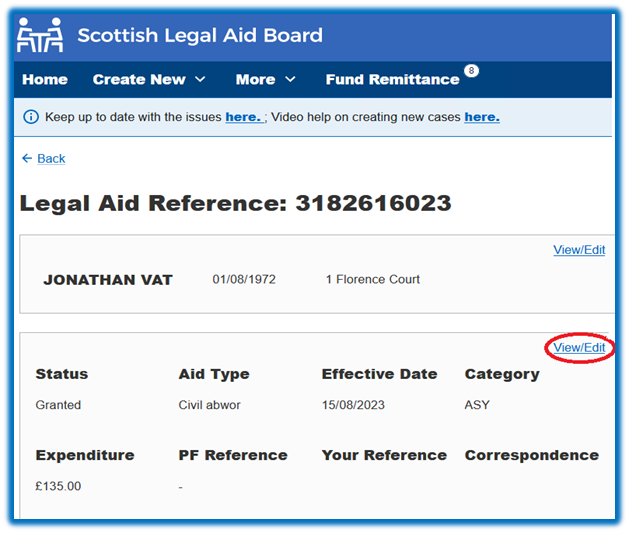

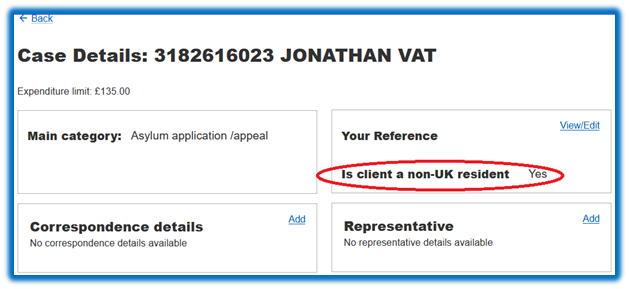

You can do this by accessing the view case function within Legal Aid Online (LAOL) and clicking on the view/edit function as shown in the screenshot:

This opens up the screen shown below where you can check the answer/update provided.

Please note it is currently not possible to edit the answer to this question – see further comments below.

As you are currently unable to edit this it is imperative that you contact us prior to drafting and submitting your account. This will allow us to make the necessary change, where appropriate. You will then be able to proceed with drafting and submitting your claim.

Where you believe you have answered the question incorrectly please contact our Helpdesk directly.

Where you believe the automatic update applied is incorrect you should email immasylum.accounts@slab.org.uk or telephone 0131 560 2159, and a member of the Accounts team will be happy to assist.

We are in the process of developing an edit feature within the Applications system which will allow you to amend the answer, where necessary, and aim to have this released as soon as possible.

For Advice and Assistance and ABWOR cases with a category of “ASY” which have been automatically updated to non-UK resident unless we are otherwise informed we will pay all accounts as VAT exempt, so it is essential that you check that the update that has been applied is correct and inform us prior to submitting your account if it is not.

In all other cases it is recognised that we will continue to receive accounts in respect of applications made before 23 September 2023, where you have not required to confirm whether your client has a right to stay in the UK.

It would therefore be helpful if at the point of submission of your account you could confirm whether your client does, or does not. have a right to stay in the UK. This is particularly important in those types of case where there may be some doubt as to your client’s residency status. Providing this information up front will help ensure prompt payment of your account.

Where it appears to us based on the information available that your account relates to legal services provided to a client who has no right to stay in the UK we will ask you to confirm what the position is before we can pay your account.

We will only make enquiry where this is necessary. We do not expect this to be required for the overwhelming majority of accounts that we receive.

Where you have confirmed at the applications stage that your client has a right to stay in the UK, or alternatively, confirmed that your client does not have a right to stay in the UK, but it appears to us based on the information available that this may be incorrect we will ask you to confirm what the position is before we pay your account.

If you have submitted an interim or final claim in respect of solicitors fees and outlays for a client who has no right to stay in the UK and this has been paid with VAT, we do not propose to take steps to recover those sums on the basis that we expect the VAT element to have been accounted for to HMRC, in the normal manner.

All accounts in respect of solicitors fees and outlays paid on or after 23 September 2023 will be paid as VAT exempt where it is confirmed, or established, that the legal services were provided to a client who has no right to stay in the UK.

This includes any case where previous payment(s) inclusive of VAT has been paid in that case.

Any subsequent payments on or after 23 September 2023 will be paid as VAT exempt so it is possible you may have some cases which have been treated differently for the purposes of VAT.